Every investing forum has the same debate: dollar-cost averaging or lump sum? I got tired of opinions, so I ran the numbers myself using 34 years of S&P 500 monthly data.

The Setup

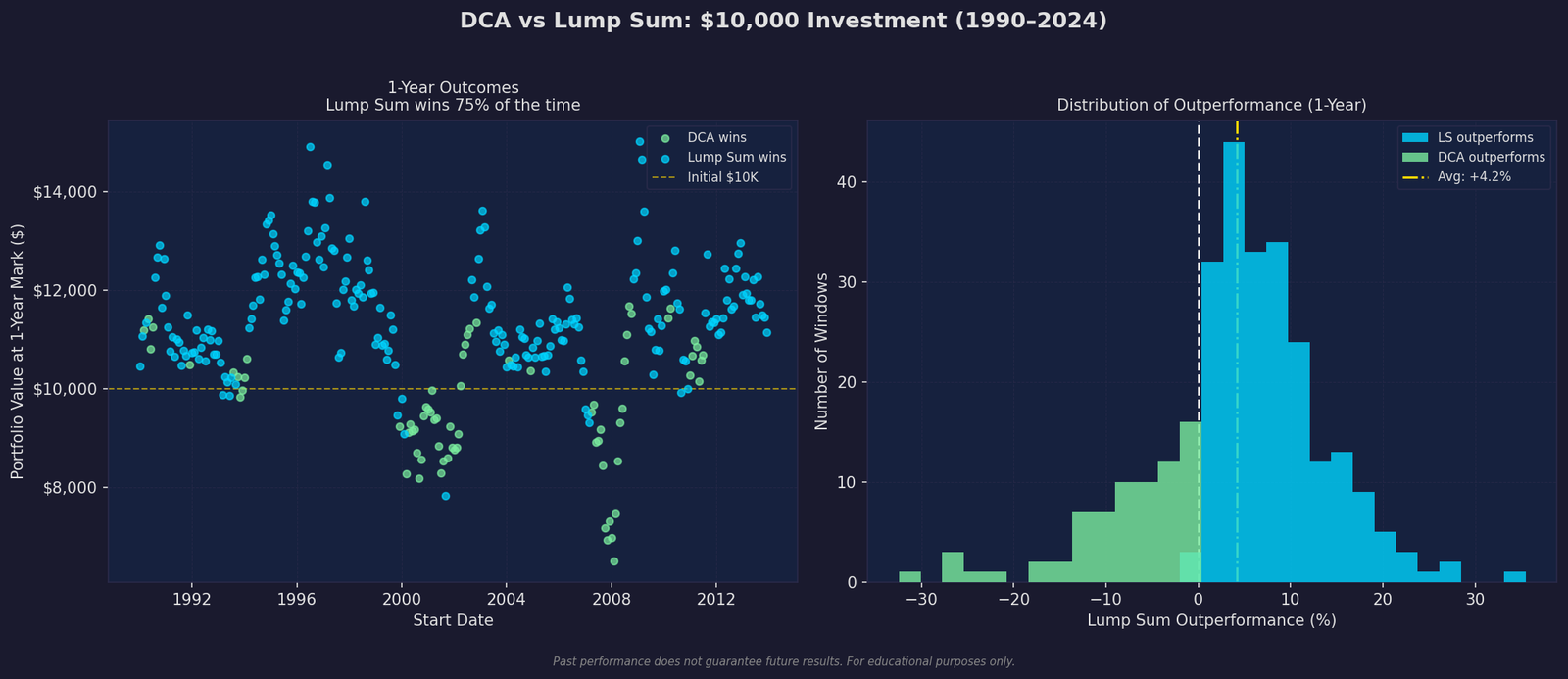

I downloaded monthly S&P 500 total return data from 1990 through 2024. For each of the 288 possible starting months, I compared:

- Lump sum: $10,000 invested on day one

- DCA: $833.33 invested monthly for 12 months

Then I measured portfolio value after 1 year and 10 years.

The Results

After 1 Year

- Lump sum wins 75.0% of the time

- Average lump sum outperformance: +4.2%

- Maximum lump sum advantage: +34.5% (investing right before a rally)

- Maximum DCA advantage: +31.4% (investing right before a crash)

After 10 Years

- Lump sum still wins 75.0% of windows

- Average outperformance grows to +7.9%

Why Lump Sum Usually Wins

Markets go up roughly 70% of the time [1]. By investing everything immediately, you capture more upside days. DCA keeps money on the sidelines earning nothing while the market rises.

The math is simple: expected returns are positive, so time in market beats timing the market.

When DCA Wins (The 25%)

DCA outperforms in one specific scenario: when you invest right before a significant decline. If you lump-summed in October 2007, you’d have lost 50% before recovering. DCA would have spread purchases across the crash, lowering your average cost.

But here’s the catch you already know: you’d have to predict the crash in advance. Nobody does this reliably. Not hedge funds, not economists, not your uncle who “called 2008.”

The Psychological Variable

The data says lump sum. But data doesn’t account for 3am panic when your portfolio is down 30%. If investing $10,000 all at once would cause you to panic-sell during a downturn, DCA is the better strategy — because the best investment strategy is the one you actually stick with [2].

My Take

I lump-sum whenever I have the money. But I’ve also held through a 40% drawdown without selling, which most people can’t do. Know yourself before you choose your strategy.

The real enemy isn’t DCA vs lump sum. It’s analysis paralysis. The difference between these strategies is ~4% over a year. The difference between investing and not investing is ~10% per year, compounding forever.

Stop optimizing entry. Start investing.

References

[1] Dimson E, Marsh P, Staunton M. “Triumph of the Optimists: 101 Years of Global Investment Returns.” Princeton University Press, 2002.

[2] Vanguard Research. “Dollar-cost averaging just means taking risk later.” 2012. vanguard.com

Disclaimer: This is educational content based on historical data analysis, not financial advice. Past performance does not guarantee future results. The backtest uses S&P 500 total return data via Yahoo Finance.